A lot can be achieved in 40 years.

You could build a decent sized Egyptian pyramid with manual labour, construct a massive channel connecting the Atlantic and Pacific oceans and still have another decade up your sleeve to develop the Apollo program to get the first man on the moon.

There would also be enough time to enjoy four weeks’ annual leave each year and three sets of accrued long service leave.

Or you could spend the time saving, just to scrape together a deposit for an average Sydney house, on an average wage.

Yes, that’s the crushing news from investment bank UBS’s economics team who have constructed a model to calculate how long it takes first home buyers to just get to the doorstep of home ownership.

Paying it off is another level of bleakness.

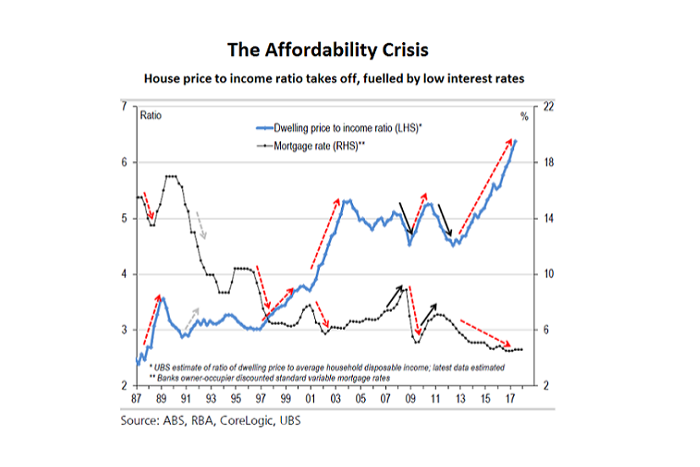

Low-interest rates have fuelled unaffordability

UBS has previously called “the top of housing” as affordability rocketed out of the realms of reasonable.

“The average house price is now six-and-a-half times the average wage. That has more than doubled in 20 years.”

Despite interest rates bumping along at historic lows, mortgage repayments are at a record high and on an alarmingly steep trajectory.

As UBS notes, the record low mortgage rates have simply been capitalised into an ever-increasing house price-to-income ratio.

As UBS notes, the record low mortgage rates have simply been capitalised into an ever-increasing house price-to-income ratio.

As it rockets away, the deposit gap for first home buyers becomes a chasm of unbridgeable proportions.

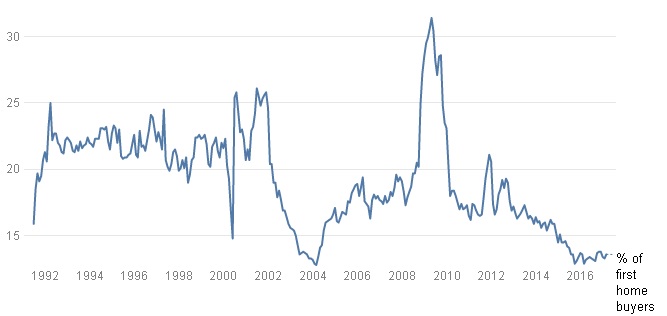

First home buyers near record lows

Not surprisingly, first home buyers’ share of all dwelling financed is close to record lows, while investors take up around half the new loans issued.

First home buyers stuck near record low share of the market

% share of all dwellings financed

The UBS equation for calculating the deposit required by first home buyers assumes several constants:

- A 10 per cent deposit is required

- Individual income is at average weekly ordinary time earnings (AWOTE) of $80,000 per year

- Saving rate is 5 percent of gross income or $4,000 per year

- Home price today is $400,000, the average first home buyer price

- Home prices grow in line with household income ahead at 3 per year

Plug that in, and the average, base-case time to come up with a deposit across the nation is 11 years.

Putting the average Sydney house price of $1.2 million into the equation and it would take around 40 years to save for a deposit.

Years to save for a deposit

However, that might be on the optimistic side.

Tougher regulations from the banking regulator, APRA, to make banks “unquestionably” strong may require lower loan-to-value ratios.

“If that means a deposit in the order of 20 per cent, then the average deposit gap would blow up from 11 years to 24 years, while in Sydney, well it would be around 100 years. Good luck with that.”

Of course, if while saving for a deposit house prices spiked — say like the 20 percent back in the early 2000s — well you can kick the proverbial can well down the road again.

UBS economist Scott Haslem acknowledged the problems with measuring the deposit gap across a long time period but said it still illustrated a point.

“Nonetheless, this model shows that the time to save a 10 per cent deposit — with a 5 percent saving rate on AWOTE of $80,000 per year — to buy a house at the average Australian capital city dwelling price of $820k has almost doubled from a long-run trend of around 10 years to 18 years now,” Mr Haslem said.

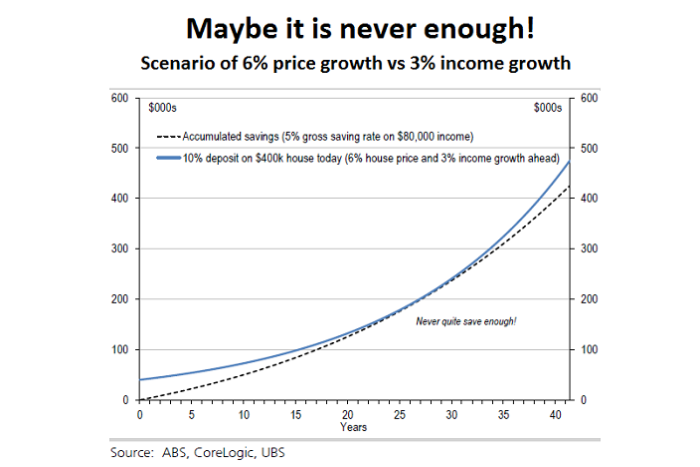

Saving may never be enough on current trends

Mr Haslem noted the key driver of the time to save a deposit was house price growth relative to income.

In the last five years, house price growth averaged 7 percent, far above household income averaging only 4 percent growth.

“Our model suggests if these trends were repeated ahead — that is an ongoing increase in the house price-income and therefore the household debt-income ratio — a potential first home buyer would likely never be able to save a 10 per cent deposit to buy a home.”

One thing the model does not calculate is which is more soul destroying, a 40-year wait scrimping to get a deposit together, or being told “forget it” and try something else.

Source: ABC News

Are you a first home buyer? Why don’t you contact one of the most reliable mortgage brokers in Australia today, call Mortgage Choice to see how they can help.